Workplace Surveillance Laws in the United States

Employee monitoring is everywhere, from email logs to biometrics. However, leaders must carefully decide what is necessary for safety and productivity and what constitutes a privacy violation.

Employee monitoring is everywhere, from email logs to biometrics. However, leaders must carefully decide what is necessary for safety and productivity and what constitutes a privacy violation.

Though brief, February was far from short on exciting news in HR tech, wellness, and benefits.

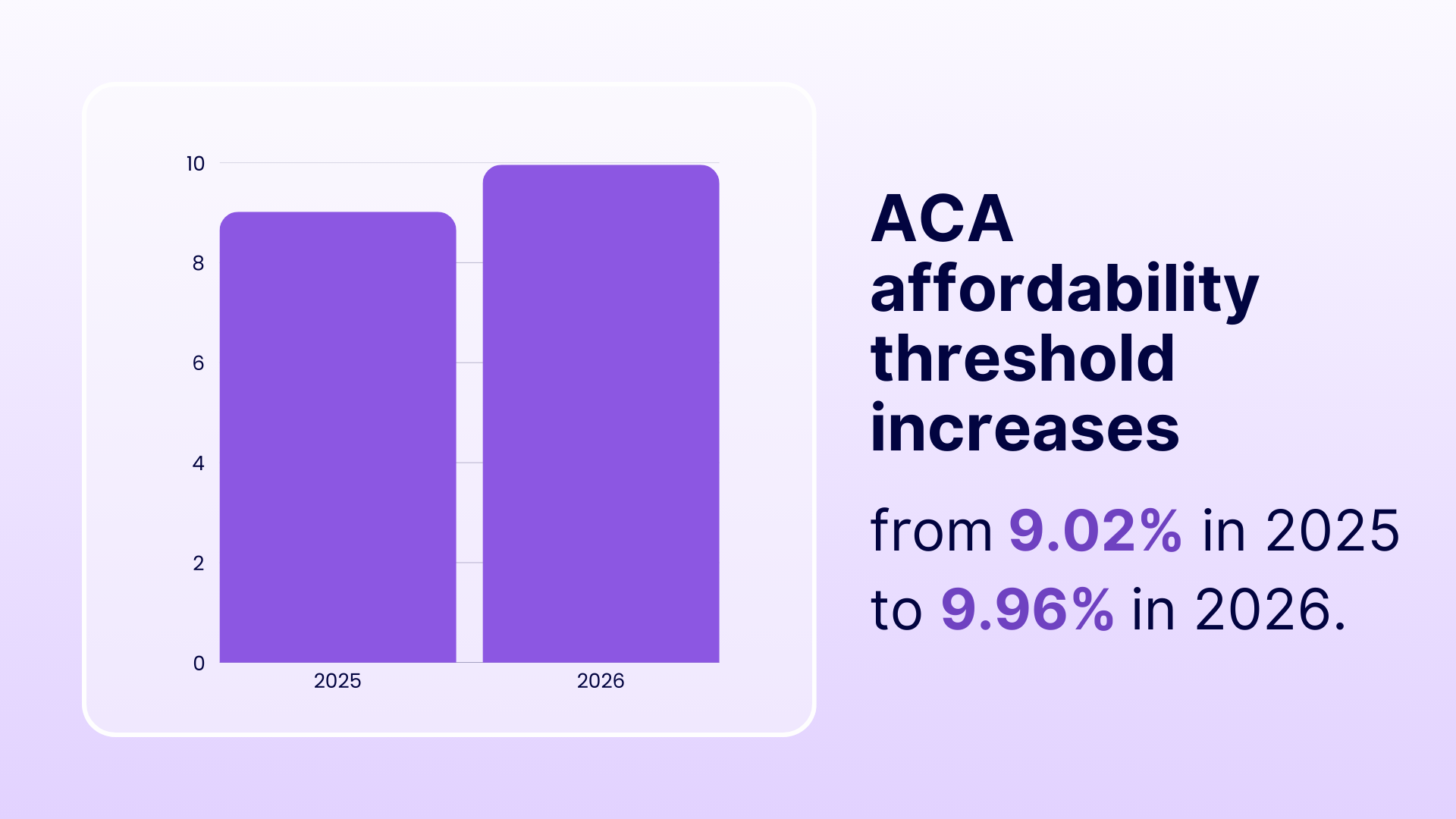

December’s HR tech, wellness, and benefits activity sits at the intersection of reflection and forecast, pointing to how the trends that defined 2025 are set to carry forward in 2026.

Their recognition of Shortlister emphasizes the platform’s dedication to providing an efficient, data-driven approach to selecting HR and benefits vendors.