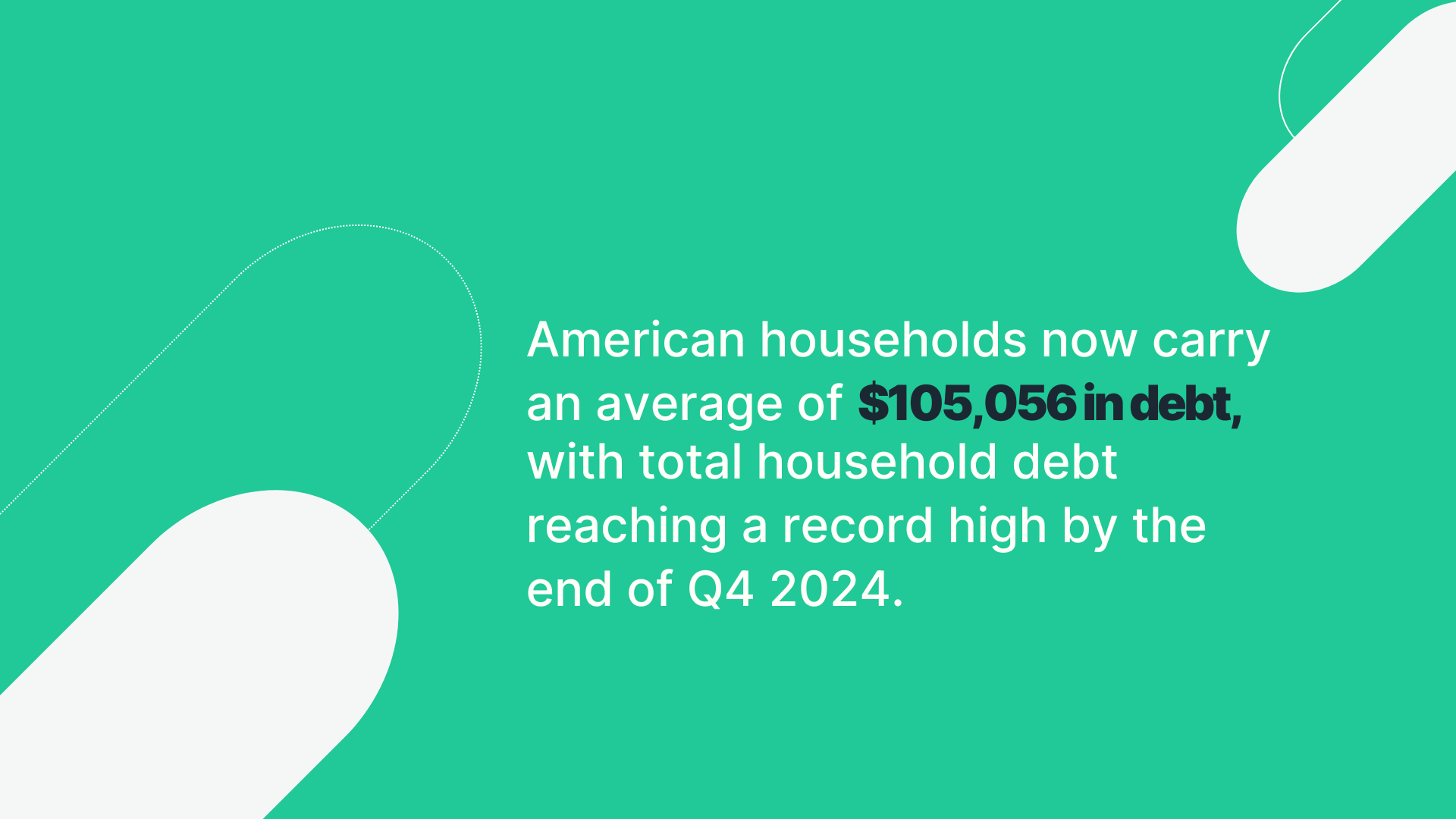

Financial decisions start early, often before people are fully prepared to make them.

For young adults (18–34), financial literacy is the foundation for healthy money habits before major life milestones.

Stefan Van der Vlag, AI Expert and Founder of Clepher, observes: “Younger generations may face challenges with managing debt and establishing a strong financial foundation during a downturn if they are not financially literate.”

Indeed, according to research from Bank of America, younger generations are mostly burdened by student debt. In fact, 24% of Gen Z and 27% of millennials had student loans in 2021.

On the other hand, middle-aged adults (35–54) are in their prime earning years and can gain a lot from financial literacy, especially when it comes to managing debt and planning for retirement.

Many in this age group also explore movements like FIRE (Financial Independence, Retire Early), using innovative investing strategies to grow their projected 401(k) value and reach financial freedom ahead of traditional retirement timelines.

Unfortunately, adults over 55 have lower rates of financial knowledge of newer financial products and are prime targets for fraud.

Increasing their understanding of finances can help protect their accumulated assets during market volatility and prepare for retirement income, healthcare costs, and legacy planning.

“A lack of financial literacy in older generations often results in difficulties managing their retirement savings and investments,” Van der Vlag adds.

“Many retirees may have relied on their company pension plans or government benefits for income during retirement, but with economic downturns affecting these sources, they may be left struggling to cover their expenses.”

That’s why financial education can’t follow a one-size-fits-all model. Instead, it must be tailored to each stage of life, income level, and financial reality to make an impact.