What is Variable Pay?

What is variable pay, and why does it matter? As financial expectations change more rapidly than traditional pay structures can keep pace, this model emerges as a potential solution to bridge the gap.

For many employees, a paycheck is the most tangible reflection of their work, and supplemental wages play a role in shaping that experience. Bonuses, commissions, annual wage supplements, or other payments that fall outside regular salaries can significantly impact their total compensation and how they perceive their employer.

While the workforce often views them favorably, any addition to regular wages can significantly increase payroll and tax complexity for the company.

Navigating this tradeoff requires a thorough understanding of the topic. Therefore, this Shortlister article focuses on the operational aspects, answering the question: What is supplemental pay, and how can you track, calculate, and report it to maintain compliance and payroll accuracy?

What does supplemental pay mean, and how does it fit into the broader definition of compensation management?

Any compensation paid beyond the employee’s regular wages or salary is supplemental pay, meaning non-base-earned pay, such as overtime, bonuses, or incentive payments.

Unlike a base salary, which is predictable and forms the core of an employee’s paycheck, supplementary payments are variable, irregular, often one-time only, or contingent on performance metrics or specific outcomes.

They are still considered taxable wages but are subject to specific tax withholding rules. Therefore, their classification at the point of payment becomes crucial for compliance and accurate payroll.

The IRS defines supplemental wages broadly. Usually they include, but aren’t limited to:

Certain taxable fringe benefits and expense allowances employees receive under a nonaccountable plan also fall under this category.

At the same time, it’s important to note that employers may choose to treat overtime pay and reported tips as regular wages rather than supplemental pay, meaning the withholding method changes, too.

Annual wage supplements, such as year-end bonuses or 13-month pay, also fall within the definition of supplemental pay when companies pay them in addition to base salaries.

The most obvious example is regular wages. These include the employee’s standard salary, hourly earnings, or other compensation the company pays consistently for each payroll period.

Vacation pay is another example, unless the employer pays it as a lump sum in addition to base pay (in which case it becomes supplemental).

Beyond these, however, not all additional payments are considered supplementary.

For instance, reimbursements made under an accountable plan are not wages, but they don’t fall under the supplementary payment category either.

Similarly, non-cash, non-taxable benefits do not qualify.

So, while it’s easy to explain what supplemental pay is and what falls under this category, it’s often harder to recognize what doesn’t, even though it’s just as important. Otherwise, misclassification can affect the way companies withhold and report these payments, making accurate taxation and payroll much more complicated.

Two payments, even with the same amount, can cause two drastically different tax outcomes depending on how payroll classifies them.

For example, a regular paycheck follows standard withholding tables tied to the employee’s Form W-4, while other forms of compensation may trigger flat rates or special calculation rules.

This distinction shapes how much tax employers withhold upfront, how payroll systems process the payment, and whether employees receive compensation in line with expectations.

With so many variables, getting classification right matters so companies can avoid errors, compliance issues, and potential employee confusion and discontent.

The main distinction lies in consistency and purpose.

Regular pay is predictable, mandatory, and forms the core of an employee’s compensation. Companies usually issue it regularly on a set pay period in a year, whether it’s weekly, bi-weekly, or monthly.

Supplemental pay, by contrast, is often variable and tied to special conditions. The employer determines which “type” to include in their compensation plan, so these are not mandatory and may be a one-time event.

Beyond these distinctions, the table below also compares other criteria, including types, taxes, and reporting.

| Regular Pay | Supplemental Pay | |

|---|---|---|

| Definition | Fixed, recurring wages that companies pay on a consistent schedule | Additional compensation, outside the normal pay cycle |

| Purpose and strategy | Compensation for regular work that reflects the terms of the work agreement | Strategic, often incentivizing performance or compensating for specific circumstances |

| Examples | Salary or hourly wages | Bonuses, commission, severance, awards, etc. |

| Withholding method | Standard wage tables based on Form W-4 | Flat rate (22%) or aggregate method, depending on payment |

| Tax rate behavior | It adjusts gradually with income | It can appear higher due to the flat or aggregate withholding method |

Supplemental wages are generally subject to federal and state income tax, Social Security, Medicare contributions, and FUTA tax, but the withholding methods differ from those for regular wages.

There are two primary approaches:

1) Flat Rate Method

This method uses a predetermined flat federal tax rate that employers apply directly to the supplemental wage, regardless of the employee’s regular tax bracket. It is most suitable for bonuses or occasional incentive payments.

2) Aggregate Method

Here, the supplemental pay is combined with the regular wage in the same payroll period, and the total is taxed at the employee’s usual income tax rate. The method is more applicable for irregular or combined payments, but it can result in higher withholding if the payment pushes the total income into a higher tax bracket.

Both methods are legally compliant, but the choice depends on payroll structure and whether income tax was already withheld from the employee’s regular wages in the current or immediately preceding calendar year.

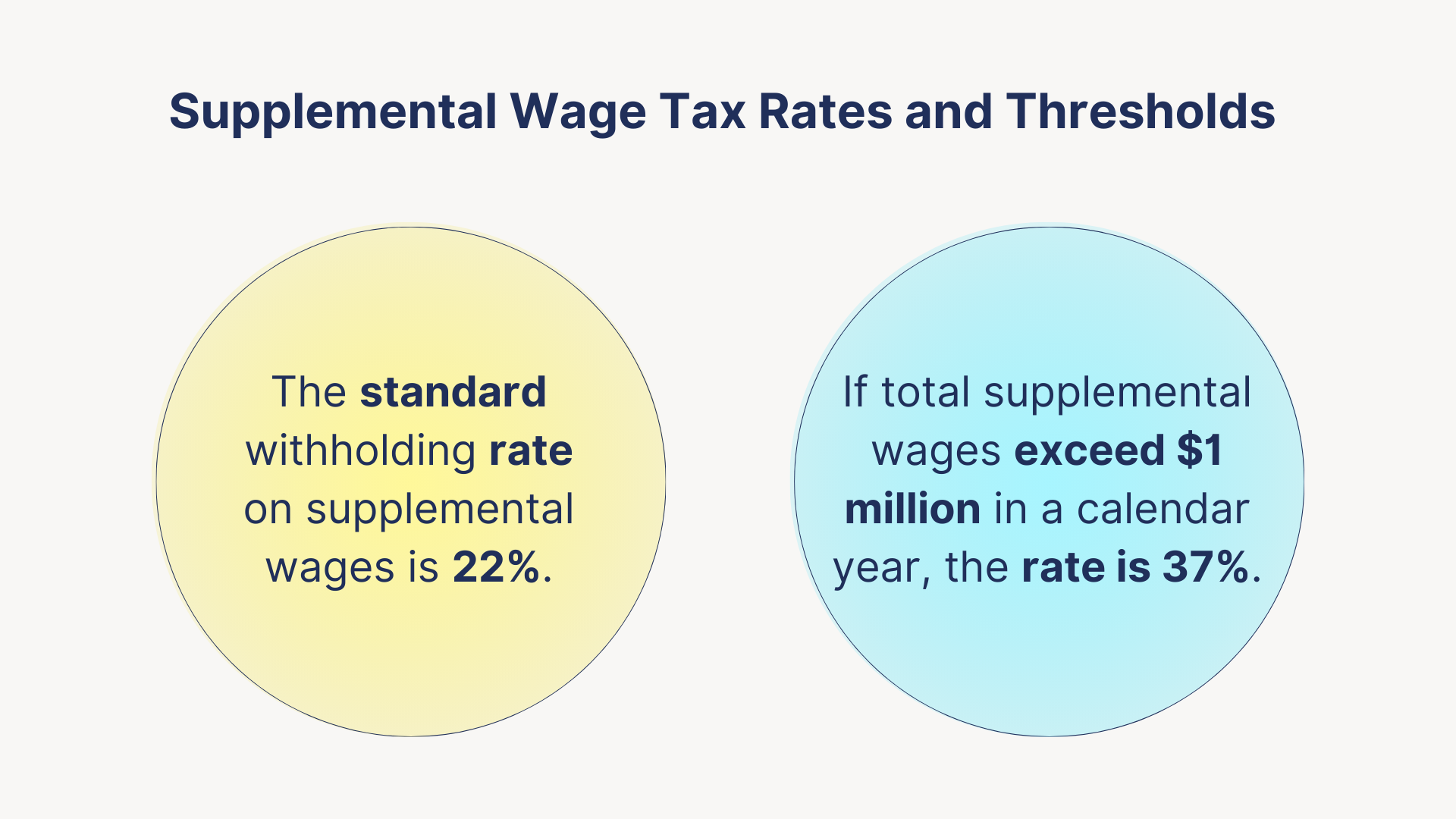

According to the 2026 IRS tax guide for employers, the federal flat withholding rate on supplemental wages remains at 22%.

However, special rules apply to high earners: payments exceeding $1 million may be subject to a 37% tax rate. When determining whether this threshold has been exceeded, employers must consider all supplementary payments made during the calendar year.

While the federal rate has remained unchanged for years, state tax rates vary significantly.

For example, some states impose a specific flat rate, such as California (10.23% bonus/stock; 6.6% other), New York (11.7%), or Michigan (4.25% flat). Other states, such as Connecticut and New Jersey, do not publish a specific supplemental rate.

A few states have no state income tax, so no withholding applies.

Under U.S. law, the responsibility for tracking, withholding taxes from, and reporting supplemental pay rests entirely with the employer.

They should report them as part of total wages on the Form W-2, in box one (wages, tips, and other compensation). Employers are also required to withhold Social Security, Medicare, and FUTA taxes on these earnings.

Since W-2 forms do not distinguish supplemental wages, employers must also ensure accuracy during payroll processing. This includes applying the correct withholding method, tracking cumulative payments for the year, and maintaining documentation on these withholdings.

The IRS offers two methods for withholding taxes on supplemental wages: a flat-rate method and an aggregate method. Choosing one is less about preference and more about how the employer identifies these payments, either separately or as part of total wages.

When a company pays supplementary wages separately from regular wages, the IRS allows them to apply the flat-rate calculation method.

The employer calculates the tax at a fixed rate of 22% of the supplemental wage amount.

For example, a worker receives a $1,000 bonus in addition to their regular wages. With this method, the employer withholds federal income tax, per IRS guidelines, totaling $220 from the bonus.

The flat-rate method is a simpler, more straightforward approach that companies usually use for one-time payments because it minimizes calculation complexity.

The aggregate method adds the supplemental payments to the employee’s regular wages from the current or most recent payroll period. The employer calculates federal tax withholding on the combined amount using the standard IRS tax tables, then subtracts the tax already withheld from the regular wages.

An example calculation is as follows:

The employee earns $2,000 in regular wages, from which $65 is withheld for federal income tax. Later in the same payroll period, they receive a $1,000 bonus.

With the aggregate method, the employer adds the bonus to the employee’s regular earnings, resulting in combined wages of $3,000. Based on the IRS wage tables, the total tax withholding on this sum is $179. From this amount, the employee subtracts the $65 already withheld from the regular wages and withholds the remaining $114 from the bonus payment.

The aggregate method ties withholding to total earnings for the pay period, so the amount withheld from the additional payment varies based on wages and Form W-4 details.

When an individual receives more than $1 million in supplementary wages in a calendar year, the employer must withhold federal income tax on the excess at the highest rate, currently at 37%. This requirement applies regardless of the employee’s Form W-4 and replaces both the flat-rate and aggregate methods for amounts above the threshold.

Supplementary pay sits outside the regular payroll rhythm.

Payments often follow different approval paths, depending on the type. They occur outside standard pay schedules and require distinct tax treatment.

As a result, the likelihood of inconsistencies increases, underscoring the need for effective management that doesn’t compromise compliance or employee confidence in payroll accuracy.

Payments that fall outside regular earnings tend to introduce complexity as they don’t usually follow standard payroll timing or structure. As a result, companies need payroll software that can distinguish between supplemental and regular wages at the point of entry. This means configuring pay codes that trigger the correct withholding logic and ensuring the system can handle both flat-rate and aggregate withholding methods.

Payroll automation is a significant consideration here, as manual overrides increase the risk of errors, particularly when these payments occur off-cycle or span multiple payroll periods.

Equally important is ensuring the payroll system can track year-to-date supplemental wages, which allows employers to monitor thresholds and maintain accurate records to avoid manual reconciliation at year’s end.

Many payroll issues originate before payroll is involved, often when the employer introduces or approves payments without a clear context.

Internal classification guidelines help answer a simple but recurring question: how should this payment be treated?

When HR, payroll, and finance share a common understanding of what supplemental pay is and how it should be processed, decisions become faster and more consistent. These documented guidelines also create continuity and a reference point, especially as teams grow or employee responsibilities shift.

Although inherently positive, any addition to an employee’s salary or tax withholding may cause confusion if the employer does not clearly communicate it. Without context, it can lead to misinterpretation and influence how workers view their overall compensation.

Instead of leaving them to speculate, companies should provide clear guidance on these payments, detailing the calculation method, the reason taxes differ from regular salaries, and exactly when the funds will appear in paychecks.

Providing the context reinforces confidence in the company’s payroll processes and supports employees’ understanding of their total compensation.

Finally, employers should regularly review cumulative supplemental wages over the year. This practice ensures the correct application of higher withholding rates when thresholds are exceeded.

Since regulations and internal practices around non-standard compensation tend to evolve, ongoing monitoring is paramount to reduce audit or compliance risks and keep compensation clear and predictable throughout the year.

Employees often judge work experience by their total compensation, especially in how bonuses, commissions, or other payments and benefits reflect the employer’s reliability and treatment of the workforce. However, they also notice how consistent and thoughtful these payments are.

Accurate classification and timely management significantly influence the employee experience, reinforcing trust in the company while maintaining compliance. Therefore, a key starting point for any employer should be to ask: What is supplemental pay, and how does it fit into the compensation strategy? With that foundation, companies can deliver pay that is both consistent and reliable.

Content Writer at Shortlister

Browse our curated list of vendors to find the best solution for your needs.

Subscribe to our newsletter for the latest trends, expert tips, and workplace insights!

What is variable pay, and why does it matter? As financial expectations change more rapidly than traditional pay structures can keep pace, this model emerges as a potential solution to bridge the gap.

When payroll errors can happen, there are ways for employees to get their money from the employer. Discover what retro pay is, how it happens, the differentiation from back pay, and its effect on taxes.

Explore how federal employee payroll deduction loans work and grasp their benefits for government employees.

Explore the perks and potential concerns of payroll tax holiday and their significance for workers and companies.

We're working hard to make it easy for you. Sign up for news, trends and insights.