How to Design an Effective Employee Incentive Plan

Are traditional financial rewards enough to motivate your team, or could the secret to unlocking peak performance lie in understanding the deeper, social value of non-cash incentives?

Outsourcing HR functions is becoming more common as companies with limited resources and human capital search to increase their efficiency and growth. Emerging as a solution to this, professional employer organizations (PEOs) are one way to combat the challenges of running a business.

These expert organizations assume an employer’s role in facilitating HR functions from payroll and benefits administration to compliance and safety measures.

Over the years, their demand has grown so much that, according to the National Association of Professional Employer Organizations (NAPEO), PEOs serve 173,000 small and mid-sized businesses.

Their relevance, not only for these but also for businesses of all types and sizes, lies in their risk mitigation and management capabilities, allowing employers to focus on other areas of business success.

This Shortlister article explores how PEOs can benefit companies in managing threats and to what extent.

A professional employer organization, or PEO, is a firm that administers different HR services on behalf of an employer. Also known as co-employment, this arrangement helps companies outsource numerous HR functions, including benefits administration, talent management, payroll, and more.

In this joint-employment relationship, a PEO acts as the employer for tax and insurance purposes, but the client company still controls the decision-making process.

Professional employer organizations help companies navigate the administrative burdens of managing a workforce by assuming one or more HR functions.

This allows the employer to focus more on its core business activities and ensures that the client company remains compliant with relevant employment laws and regulations, mitigating or managing the risk of legal and regulatory issues. Global Professional Employer Organizations (global PEOs) operate in the same way, but act as the international co-employer of global teams.

Risk mitigation is a process companies use to prepare themselves for a potential threat to their business continuity and minimize its impact. Although often used interchangeably, this is not the same as risk management, which represents a comprehensive process of identifying, assessing, and controlling risks in the workplace.

Instead, risk mitigation prioritizes an identified threat.

Its goal is to lessen the likelihood or aftermath of the risk.

For example, companies can partner with a PTO to minimize legal penalties and lawsuits to maintain compliance with employment laws. This is called risk sharing, as it involves third parties sharing the responsibility of a potential threat.

Other risk mitigation strategies may include:

Overall, what approach companies or co-employment PEOs take to tackle threats to business continuity depends on knowing the type of workplace risk they face.

When this isn’t an option, they should turn to risk management.

There’s no such thing as a perfect or risk-free work environment.

Regardless of the cause or reason, every workplace comes with a risk for the employer and its employees.

Sometimes, these threats can be traced to external factors, such as a volatile economy, regulatory changes, and market fluctuations.

More often, it’s human error.

Mistakes, negligence, inexperience, and misjudgment are all fundamental sources of risk in business operations and can lead to work inefficiencies, financial losses, and even reputational damage.

A more precise classification by the Occupational Safety and Health Administration (OSHA) recognizes six types of workplace risks, which can all be traced back to human error, accidents, or external factors:

Failure to mitigate these examples can significantly harm the organization and its employees. The fact that each hazard differs shows that any industry, company, or work environment inherently brings a risk element.

Consequently, employers turn to risk mitigation strategies.

Outsourcing a PEO, for example, can help them set up policies in adherence to law regulations and procedures that address some or all of the risks mentioned above. Moreover, with their expertise, professional employer organizations can facilitate preventative programs to track and quickly address any issues, reducing the threats of accidents, injuries, and more.

This can help companies better prepare for any long-term effects on their prosperity and the well-being of their employees, creating a safe and productive environment.

No matter how good of a mitigation strategy employers follow, sometimes threats and their consequences can’t be avoided, which is when they should turn to risk management.

Running a business is challenging, between managing the workforce, remaining compliant, and understanding the inherent nature of workplace risk. This is particularly true for small and mid-sized companies with limited resources, which is why they usually outsource many business operations.

PEOs have shown to be helpful for business owners who want to streamline their administrative tasks, including:

The services they outsource depend on the PEO and the contract with the employer.

Risk management is just one aspect they cover.

However, once this co-employment is established, with each HR function they take over, a portion of workplace risks and liabilities naturally shift to PEOs.

Personal employer organizations then use their expertise to mitigate the risks. If that’s unfeasible, they turn to risk management and strategic guidance to help businesses respond to and recover from threats.

A PEO will primarily focus on risk mitigation strategies to proactively prevent and reduce potential threats, for example, taking over compliance, HR management, or employee training.

However, a standalone aspect of PEO coverage is risk management, or helping companies detect, respond to, and recover from a risk that has already occurred.

Setting up the right strategy to help the client company depends mainly on the contract or what services the employer needs. The process for this, however, goes through several phases:

Before we go in-depth into each key area of PEO risk management, let’s explore why they are a good idea for businesses looking to streamline their operations.

Taking over critical and time-consuming operations and their inherent risks is one way PEOs benefit companies. However, their advantages go beyond this.

Statistics show that companies that employ professional employer organizations have 40% better revenue growth, up to 16% lower turnover, and are half as likely to go out of business.

In fact, PEO benefits expand to:

Ultimately, PEO risk management benefits overlap with the overall advantages since employers can leverage invaluable expertise and resources to manage HR-related risks through this partnership.

Now that we know what a professional employer organization is and how it benefits companies let’s take an in-depth look at the key areas of PEO risk management and what they mean for organizations.

As an essential tool for businesses seeking to safeguard their long-term growth, PEO helps them identify potential risks, assess their likelihood of impact, and develop strategies to manage them.

From Workers’ Comp to HR compliance, these are the key areas of PEO risk management.

PEOs typically assist companies with workers’ compensation, an insurance that provides employees with wage replacement and medical care in case of a work-related injury or illness. Beyond assistance, their job also includes guaranteeing compliance with complex legal requirements from federal and state laws.

Failure to do this can lead to severe legal consequences and financial repercussions for the company. Thus, this co-employment helps business owners manage employee claims effectively, handle paperwork, and offer up-to-date and timely coverage.

Although there are ways to mitigate injuries and illnesses, there isn’t a bulletproof solution to prevent them entirely in the workplace. Thus, companies turn to the alternative of risk management.

As mentioned above, handling claims is an aspect of Workers’ Comp that PEOs can take over. In this case, their responsibilities expand to simplifying the reporting process for employees, coordinating medical care, keeping insurance costs in check, dealing with paperwork, and more.

With this, professional employer organizations help reduce many legal, financial, and operational risks.

“To assure safe and healthful working conditions for working men and women; by authorizing enforcement of the standards developed under the Act; by assisting and encouraging the States in their efforts to assure safe and healthful working conditions; by providing for research, information, education, and training in the field of occupational safety and health.”

This is an excerpt from the Occupational Safety and Health Act (OSHA) of 1970. Its goal is to ensure a working environment that protects the health and safety of the workforce.

The OSHA has expanded employer responsibilities and violations in the past decades since its implementation. Thus, beyond claims and compensations, OSHA compliance is another risk management aspect regarding injuries and illnesses that occur in the workplace.

Using the OSHA 300 form, employers annually record and summarize workers’ injuries and illnesses. However, they can outsource this task to PEOs, which then assume the responsibility of recordkeeping, removing the risk of incorrect reporting.

Beyond the OSHA 300 Log, they develop and update safety manuals, coordinate safety training, and conduct audits and inspections to find and correct any safety and health hazards.

The cost of substance abuse in indirect productivity loss goes up to $207 billion. Of those, 89% are driven by health-related categories.

Apart from the financial repercussions, substance abuse in the workplace can significantly impact the safety of employees. For example, it can impair judgment, coordination, and cognitive abilities, leading to possible workplace accidents and endangering the well-being of the entirety of the workforce.

As a significant risk, PEOs can assist in risk management by helping businesses implement proactive substance abuse programs, including:

Another key area of PEO risk management is loss prevention, which refers to a strategy or multiple strategies that aim to reduce or prevent losses of company assets and revenue.

In this context, the role of professional employer organizations is to implement security measures and monitoring on behalf of their client company. For example, they can install security cameras, systems, and protocols. However, before doing this, they also conduct risk assessments to identify the proper strategy and resource allocation for this type of risk management.

These loss prevention measures should minimize the probability of risks like potential theft, security breaches, and even vandalism. The end goal, however, is to create a culture of awareness and accountability among the workers, mitigating future risks of internal theft.

We can discuss policies, programs, and strategies to manage risks and safety concerns. However, without involving the workforce, these all fall short regarding their long-term effectiveness.

To manage yet another risk, PEOs can take over the facilitation of employee training on different safety and health concerns. That involves providing resources and educating workers on workplace safety measures, emergency procedures, and compliance with regulations.

The goal is to empower employees with the knowledge and tools to address and prevent risks themselves, leading to a culture of proactive risk management that can, in the long run, create a much safer work environment.

Employee policies aim to set clear rules and expectations for employees, outlining their legal obligations and rights. In collaboration with the employer, PEOs leverage their knowledge and experience in developing these policies and comprehensive employee handbooks on safety, employee conduct, and compliance. They also align the policies with legal requirements and industry norms.

As a risk management strategy, this could protect the company from lawsuits while protecting its workers from discrimination, wrongful termination, or other threats.

According to the U.S. Equal Employment Opportunity Commission (EEOC), 2022 discrimination charges reached 73,485, a 20% increase from the previous fiscal year. There was also an 18% increase in calls and 32% more emails regarding workplace discrimination.

It’s safe to conclude that prejudice based on age, gender, religion, race, or disability is still a significant issue in the workplace.

When companies fail to address it, it also becomes a legal liability.

Harassment, defined by EEOC as a form of employment discrimination, becomes unlawful when:

To prevent the risk of this happening, professional employer organizations provide anti-discrimination and harassment training to employees to educate them on unlawful and inappropriate behavior. Aside from avoiding legal disputes, the end goal is to help companies create and promote a culture of inclusion and diversity.

Emergency response planning is a comprehensive, documented strategy that includes specific actions and timeframes in the case of a critical event. It ensures the safety of the workforce and minimizes the event’s impact on the businesses.

By outsourcing this to a PEO, companies get assistance in creating and implementing this plan, including:

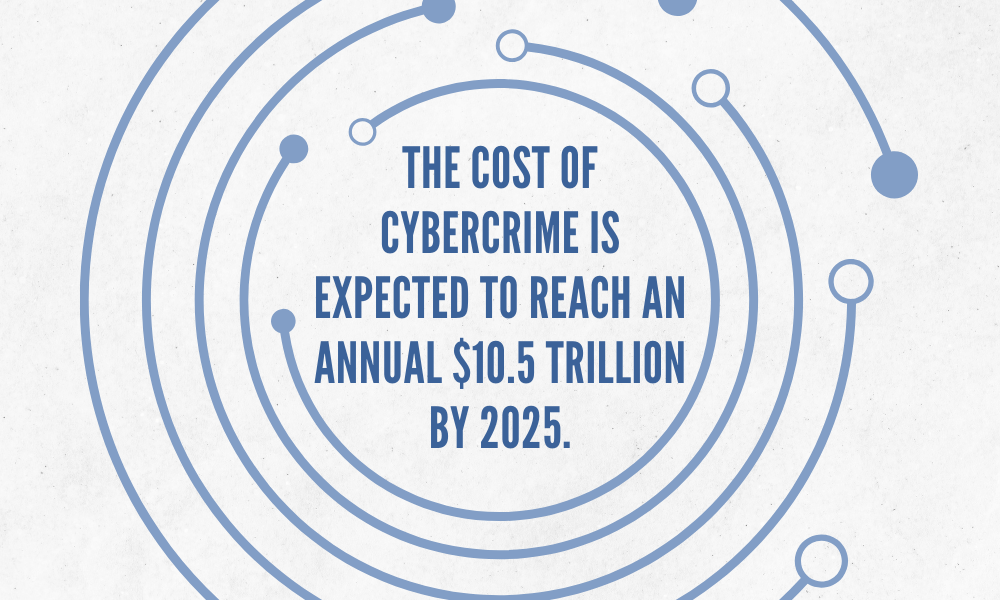

In this digital economy, data is everything.

Research by the IBM Institute reveals that companies with the most advanced security approach and capabilities had 43% higher revenue growth over five years.

However, along with the digital and technological revolution came cyber threats, whether in the form of malware, spam and phishing, or data breaches. In fact, IBM also shows that the cost of cybercrime is expected to reach an annual $10.5 trillion by 2025.

Since it has become increasingly challenging to mitigate, companies that lack the right resources and teams outsource this type of risk management to professional employer organizations. In return, PEOs conduct risk assessments, develop policies, provide employee training, recommend technology, and prepare a response to a potential cyber-attack.

Finally, HR compliance stands as a roundup of everything we mentioned above. It means ensuring that what the company does and implements is adherent to local, state, and national labor laws.

While we have already glanced at compliance at some of the other key areas of PEO risk management, HR compliance is a comprehensive process that involves evaluating all company HR policies, employment, payroll, health and safety, disability structure, discrimination policies, and more.

An ADP survey shows that 70% of small businesses have ad hoc HR managers.

Of those, only one in four is confident that their business is fully compliant. This significant risk can be managed by employing professional employer organizations to take over HR tasks and conduct audits to identify potential compliance gaps.

Regular audits ensure the company mitigates or efficiently manages risks by keeping it up to date with changing laws, reducing the likelihood of hefty fines.

PEO awareness and usage are growing.

According to PRNewswire, awareness of these organizations has increased by 48% since 2018, and there was also an increase in their usage, with a record 33% of decision-makers using a PEO. Of those who currently don’t employ one, 81% reported being interested in using one in the future.

Moreover, in 2022, the market size for PEOs was valued at $62.66 billion, with estimates that it will reach $158.99 billion by 2031 globally.

This growth is attributed to the demand for outsourcing HR services.

With the added benefit of risk mitigation and management, professional employer organizations have become a go-to option for companies of all sizes as they seek to streamline their operations and focus on core business functions.

Content Writer at Shortlister

Browse our curated list of vendors to find the best solution for your needs.

Subscribe to our newsletter for the latest trends, expert tips, and workplace insights!

Are traditional financial rewards enough to motivate your team, or could the secret to unlocking peak performance lie in understanding the deeper, social value of non-cash incentives?

Gain valuable insights into diverse cultural examples and understand their pivotal role in fostering a thriving, motivated workforce.

“What gets measured gets managed” is a familiar business principle. When it comes to pay equity, however, most companies still fall short.

Dress codes have gone vague and viral. But could your look be quietly costing you trust, influence, or even a lawsuit?

We're working hard to make it easy for you. Sign up for news, trends and insights.