What is a Payroll Tax Holiday?

Explore the perks and potential concerns of payroll tax holiday and their significance for workers and companies.

When an employee’s debt goes unresolved, the obligation to recover it can land squarely with the employer, not by choice, but by law. A formal notice arrives, instructing them to deduct a portion of that employee’s wages and remit it to the relevant authority.

If the company operates in the United States, this is called a wage garnishment.

If it operates in the United Kingdom, it’s a direct earnings attachment (DEA). This mechanism has a different name and framework, but the core obligation is the same.

Understanding both is increasingly important as companies manage workforces across borders, use U.K.-based payroll systems, or evaluate their compliance processes against international standards.

This Shortlister article explains what direct earnings attachment is, where it applies, how it works in practice, and what the U.S. equivalent looks like.

A direct earnings attachment, commonly referred to as a DEA, is a legal mechanism that allows debt collection by instructing an employer to deduct amounts directly from an employee’s wages, without needing a court order.

It’s a U.K.-specific process used by the country’s Department for Work and Pensions (DWP), or, in some cases, a local authority to collect debts arising from benefit overpayments. Authorities use it when they have already tried other recovery methods but haven’t been able to collect the debt.

In plain terms, the direct earnings attachment meaning is this: a government body has identified that an individual owes money for an overpaid social security benefit, has been unable to recover it voluntarily, and is now instructing the employer to recover it from the individual’s wages on the government’s behalf.

DEAs currently only apply in England, Scotland, and Wales, but not in Northern Ireland, the Channel Islands, or the Isle of Man.

In the United States, the functional equivalent of a DEA is wage garnishment.

However, this is a broader process, with differences in legal authority, court involvement, deduction limits, and employer obligations. Recognizing where these two align and where they differ can help clarify responsibilities for companies operating across jurisdictions.

Wage garnishment is a legal process that requires an employer to withhold a portion of an employee’s earnings to satisfy a debt.

In most cases, garnishment in the U.S. follows a court judgment obtained by a creditor. Once a court issues an order, the employer must calculate the permissible withholding amount and remit payments as directed.

Common forms of wage garnishment include:

Not all garnishments require a traditional court judgment. Certain federal and state agencies have statutory authority to initiate administrative wage garnishments, meaning they can order withholding without first filing a lawsuit. In that sense, they are the closest parallel to DEAs. For example:

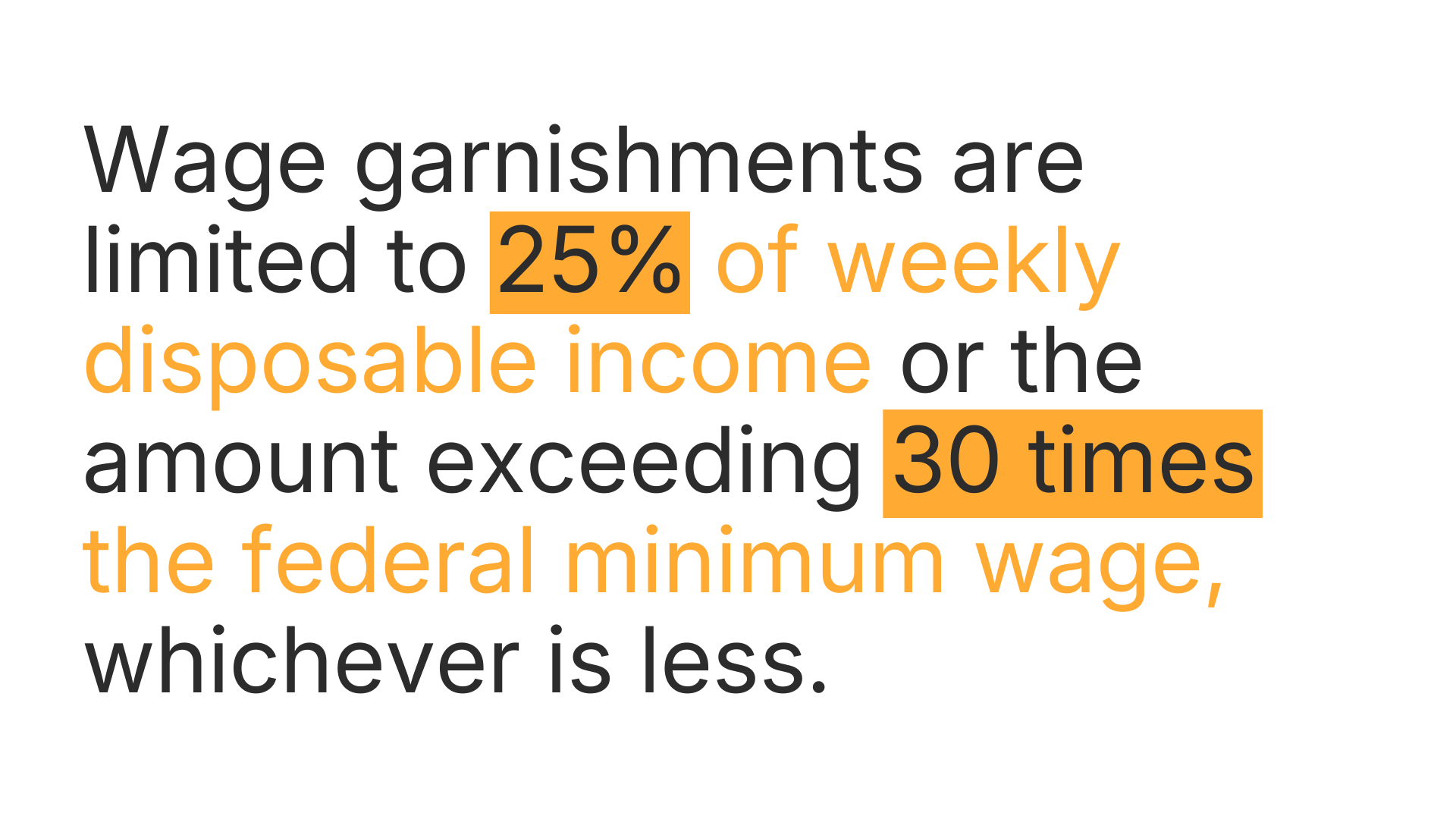

Federal law, primarily Title III of the Consumer Credit Protection Act, limits the amount that can be garnished in most creditor cases. Withholding is capped at whichever is less: 25% of disposable earnings, or any earnings above $217.50 per week – a figure representing 30 times the federal minimum wage of $7.25 per hour.

It also protects employees from being fired by their employers because their wages have been garnished for any one debt. Child support and tax levies are subject to different statutory limits.

Employers are legally obliged to comply with wage garnishment orders and may face penalties for failure to withhold or remit funds as required.

The main structural difference between a direct earnings attachment and a U.S. wage garnishment is that DEAs are issued directly by a government agency without court involvement. In contrast, most garnishments require a court order first (with some exceptions).

Both systems place the employer squarely in the middle, obligating them to calculate, withhold, and remit deductions on time and accurately.

The following comparison provides a useful reference point.

| Factor | DEA (UK) | Wage Garnishment (US) |

|---|---|---|

| Issuing authority | Department for Work and Pensions or local authority | Courts, IRS, state agencies |

| Court order required | No | Yes, with some exceptions |

| Governing legislation | Welfare Reform Act 2012; Social Security (Overpayment and Recovery) Regulations 2013 | Consumer Credit Protection Act, Title III; state laws |

| Applies to | Benefit overpayments and specific public debts | Consumer debts, taxes, child support, student loans |

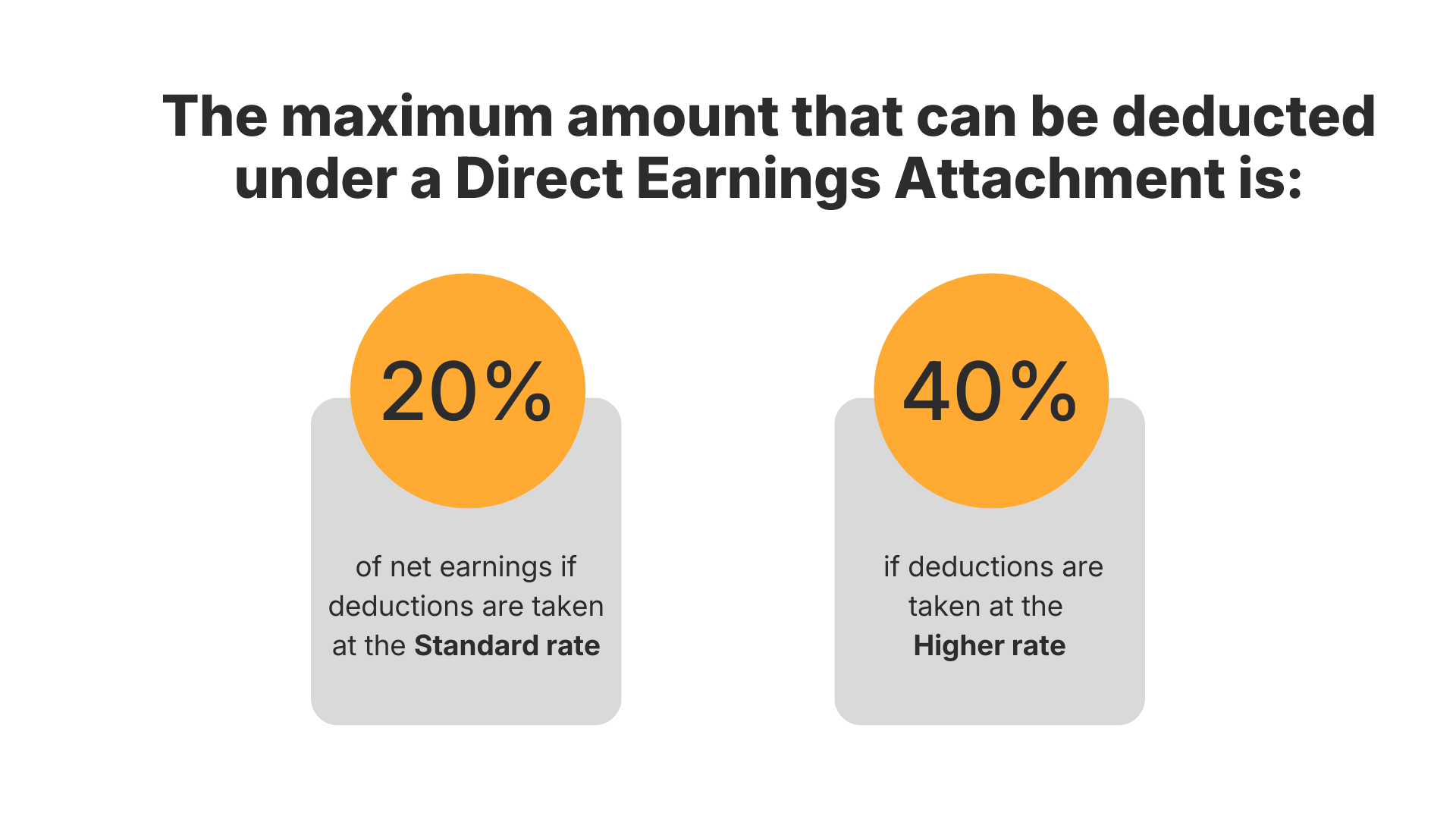

| Maximum deduction | 20% (standard rate) or 40% (higher rate) of net earnings | Usually 25% of disposable earnings, but child support and taxes have separate caps |

| Protected earnings floor | 60% of net earnings | Amount equivalent to 30x the federal minimum wage per week ($217.50 per week) |

| Employer admin fee | Up to £1 per pay period | Varies by state and garnishment type |

| Employee termination protection | Not specified within the DEA regulations | Prohibited for garnishment arising from a single debt |

For most U.S.-based employers, a DEA notice will never arrive in the mail.

The framework was introduced as part of the U.K. Welfare Reform Act of 2012, giving the DWP a faster and more direct route to recover overpayments without relying on court proceedings.

However, that does not mean it is not relevant, particularly for those with employees and operations in the United Kingdom or companies using U.K. payroll platforms.

Beyond direct exposure, understanding the meaning of direct earnings attachment is useful because it illuminates a category of payroll obligation that most HR professionals in the United States already manage under a different name. At the same time, knowing the difference can help avoid confusion (for companies and employees) and ensure multi-state payroll compliance.

A direct earnings attachment can feel sudden for employees, even though it follows a clear procedure.

It begins when the Department for Work and Pensions identifies a benefit overpayment without a voluntary repayment plan in place. At that point, the DWP Debt Management intervenes and issues a formal notice to the employer with instructions.

From there, the employer calculates the deduction based on net earnings, applies it through payroll, and sends the amount to DWP. The exact process repeats each pay cycle until the debt gets cleared, the DWP issues a stop notice, or the employee leaves the company.

Notably, the regulations state that the employer must inform the employee of the amount of the deduction, including any administration costs, and the calculation method. Often, they include this information on the payslip.

The process is simple enough to follow: calculate the deduction, apply it through payroll, and remit it to the DWP.

But how does an employer know to calculate the direct earnings attachment?

With a DEA deduction, employers apply a percentage of the employee’s net earnings, which is their take-home pay after deducting income tax, National Insurance, and pension contributions.

The DWP sets the percentage rate, using one of two options: Standard Rate (Table A) or Higher Rate (Table B). It also specifies which to use when it issues the notice (the employer has no say in this).

Both tables are tiered, and the more an employee earns, the higher the percentage applied.

The Standard Rate ranges from 0% to 20% and the Higher Rate ranges from 5% to 40%. For example, an individual with monthly net earnings of £960 would face a deduction of 7% under the Standard Rate (£67.20) or 14% under the Higher Rate (£134.40).

This calculation follows three steps:

Importantly, the employer must also consider the “protected earnings” amount, which equals 60% of an employee’s net earnings. Specifically, this means that after adding the DEA deduction to any other orders already in place, the employee must take home at least 60% of their net wage each pay period.

Not everything an employee receives in their compensation counts as earnings for DEA purposes. This distinction matters because the deduction is calculated only against qualifying earnings.

| What counts as earnings? | What does not count as earnings? |

|---|---|

| Wages, salary, and fees | Statutory family pay (maternity, paternity, adoption, shared parental pay) |

| Bonuses, commissions, and overtime pay | Pension, benefits, and credit paid by the DWP, local authority, or His Majesty’s Revenue and Customs (HMRC) |

| Statutory sick pay and compensation payments | Redundancy payments and reimbursed expenses |

| Occupational pension (paid with wages) | Military pay and allowances |

| Payment in lieu of notice | Payments from public departments outside the United Kingdom |

When in doubt, employers should refer to the full list of qualifying earnings in the DWP’s detailed guidance. Otherwise, getting this wrong affects the accuracy of every deduction.

The U.S. wage garnishment framework draws a similar distinction.

The amount subject to garnishment is based on an employee’s disposable earnings, defined as the amount left after legally required deductions. Meanwhile, deductions not required by law, such as voluntary retirement plan contributions or health insurance premiums, are not subtracted from gross wages when calculating disposable earnings.

Once you receive a formal notice, the obligations are real, time-sensitive, and carry consequences for non-compliance. According to guidance by the Department of Work and Pensions, the following are employers’ core responsibilities when obtaining a DEA notice:

Failure to comply can result in a fine of up to £1,000.

By comparison, the U.S. framework is slightly simpler, focusing mainly on capping the amount withheld and protecting employees from dismissal.

Processing deduction orders creates administrative work for employers, which justifies them charging a fee. In fact, data shows that 40% of all employers who are aware of the administrative levy apply it.

However, there are some limitations.

Firstly, the administrative fee is capped at £1.00 per deduction period, regardless of the size or complexity of the deduction. Employers can take it even if it reduces the employee’s income below the 60% protected earnings amount, provided it does not reduce their pay below the national minimum wage.

Moreover, the £1.00 can only be charged when an actual deduction is made and remains the same amount, even if multiple pay periods are combined into a single deduction.

In the U.S., the ability to charge an administrative fee depends on state law and the type of garnishment. For example, under Virginia law, employers (garnishees) can charge employees up to $10 per garnishment summons processed.

This scenario is one of the more operationally complex tasks HR and payroll teams face.

When an employee carries multiple deduction orders, employers must apply them in a specific sequence.

In the U.K., there’s a hierarchy of priority.

For example, in England and Wales, child maintenance, court-ordered earnings deductions, and council tax all take priority over other deductions. Scotland has its own equivalent priority orders, but the principle is the same: certain debts, particularly child maintenance, always come first.

Regardless of the order, the “protected earnings” rule still applies. In other words, the combined deductions shouldn’t push the employee’s take-home pay below 60% of net earnings.

In the U.S., the CCPA sets an absolute ceiling on total garnishment regardless of how many orders exist, but does not itself determine priority between competing orders. Priority among multiple garnishments is determined by state law or other federal statutes.

For an employer, deducting a portion of someone’s wages is a payroll entry.

For the employee, it’s a direct reduction in the income they rely on to meet everyday financial obligations.

Yet, the law does not leave them without recourse.

In the U.K., no combination of DEA deductions and other orders can reduce a worker’s take-home pay to less than 60% of their net earnings in any given pay period.

Employees who believe the amount owed is incorrect or that the deduction amount is wrong have the right to challenge it. The first step is contacting DWP Debt Management directly to dispute the DEA. If the issue remains unresolved, they can then escalate their dispute to the relevant ombudsman.

In the U.S., the CCPA establishes a federal baseline. Most notably, it prohibits an employer from firing an employee “whose earnings have been subject to garnishment for any one debt, regardless of the number of levies made or proceedings brought to collect that debt.”

For those navigating either system, knowing that rights exist is the first line of defence.

HR teams are well-positioned to play a supportive role here by communicating clearly with affected employees, advising on available dispute-resolution processes, and handling the situation with discretion.

A DEA places the administrative burden on the employer.

However, in practice, the majority of this responsibility falls on HR and payroll teams, from understanding what direct earnings attachment is (or its U.S. equivalent), to getting the calculation right, applying the correct rate, respecting the protected earnings threshold, and remitting on time.

The consequences of getting any of the steps wrong extend in both directions: financial penalties for the business and financial hardship for the employee.

Several practical approaches can make this responsibility more manageable.

The first is a reliable payroll software that accurately handles both DEA and garnishment calculations. This means including the correct application of protected earnings thresholds, administrative fee logic, and multi-order prioritization.

Another consideration is aligning internal processes. Who receives a direct earnings attachment or wage garnishment notice? Who calculates the deduction? Within what timeframe? Who communicates with the employee and who remits payment? Without a defined workflow, risk increases with each notice received.

Finally, regulations, rates, and individual circumstances all change over time. Meanwhile, the DEA framework and the U.S. garnishment system are two examples of how different legal environments impose distinct obligations on employers that share the same fundamentals. Therefore, payroll compliance becomes increasingly important and should be reviewed regularly, especially for employers with a global workforce.

A DEA is, by definition, a debt recovery mechanism. But understanding what a direct earnings attachment is in practice reveals a more complex reality. Behind every notice is an employer with a regulatory obligation, an employee with legitimate concern, and an HR and payroll team working to support both. Getting this balance right is not just about good compliance, but about good management.

Content Writer at Shortlister

Browse our curated list of vendors to find the best solution for your needs.

Subscribe to our newsletter for the latest trends, expert tips, and workplace insights!

Explore the perks and potential concerns of payroll tax holiday and their significance for workers and companies.

Explore the ins and outs of running payroll and the different methods and payroll services businesses use to compensate their employees.

Learn how pre-tax deductions can be a great work perk to get many company benefits and insurance while saving money.

Payday might feel like just another date on the calendar, but it’s the difference between stability and stress for millions of employees.

We're working hard to make it easy for you. Sign up for news, trends and insights.